Four signals that matter from MWC’s Satellite & NTN Summit

20 Mar 2026

Insights for systems integrators and solution providers from the GSMA Satellite & NTN Summit at Mobile World Congress Barcelona 2026. The whole session is available to watch on YouTube here.

Author: Nicole Russo, VP Commercial Operations, Myriota

The GSMA’s Satellite & NTN Summit at MWC Barcelona has become something of a barometer for the industry’s mood. A few years ago, sessions were still weighted toward possibility – what NTN could become, which standards might land, and whether operators would ever take satellite seriously. This year felt meaningfully different. The room was standing-room-only, and CEOs from major operators put satellite front and center, citing it as a customer priority. The conversation has shifted from “if” to “how fast.”

Myriota’s COO George Kanuck joined industry leaders – including representatives from the European Space Agency, the Global Satellite Operators Association, major MNOs from Japan and Ukraine, and satellite partners like Viasat – for a packed morning of panels and keynotes.

For systems integrators and solution providers working to deploy satellite IoT connectivity at scale, the summit contained some important signals – both encouraging and clarifying. Here’s what stood out.

1. NTN has crossed from ‘nice to have’ to ‘must have’ – but the real scale is in IoT

GSMA Intelligence opened the summit with a pointed observation: a year ago, having an NTN strategy was optional for mobile network operators. Today it’s a board-level priority. Around 70% of global telco market share now has at least one satellite partnership in place, up substantially from the year prior – a shift Tim Hatt, Head of GSMA Intelligence, described as moving from pragmatic experimentation to genuine commercialisation at scale.

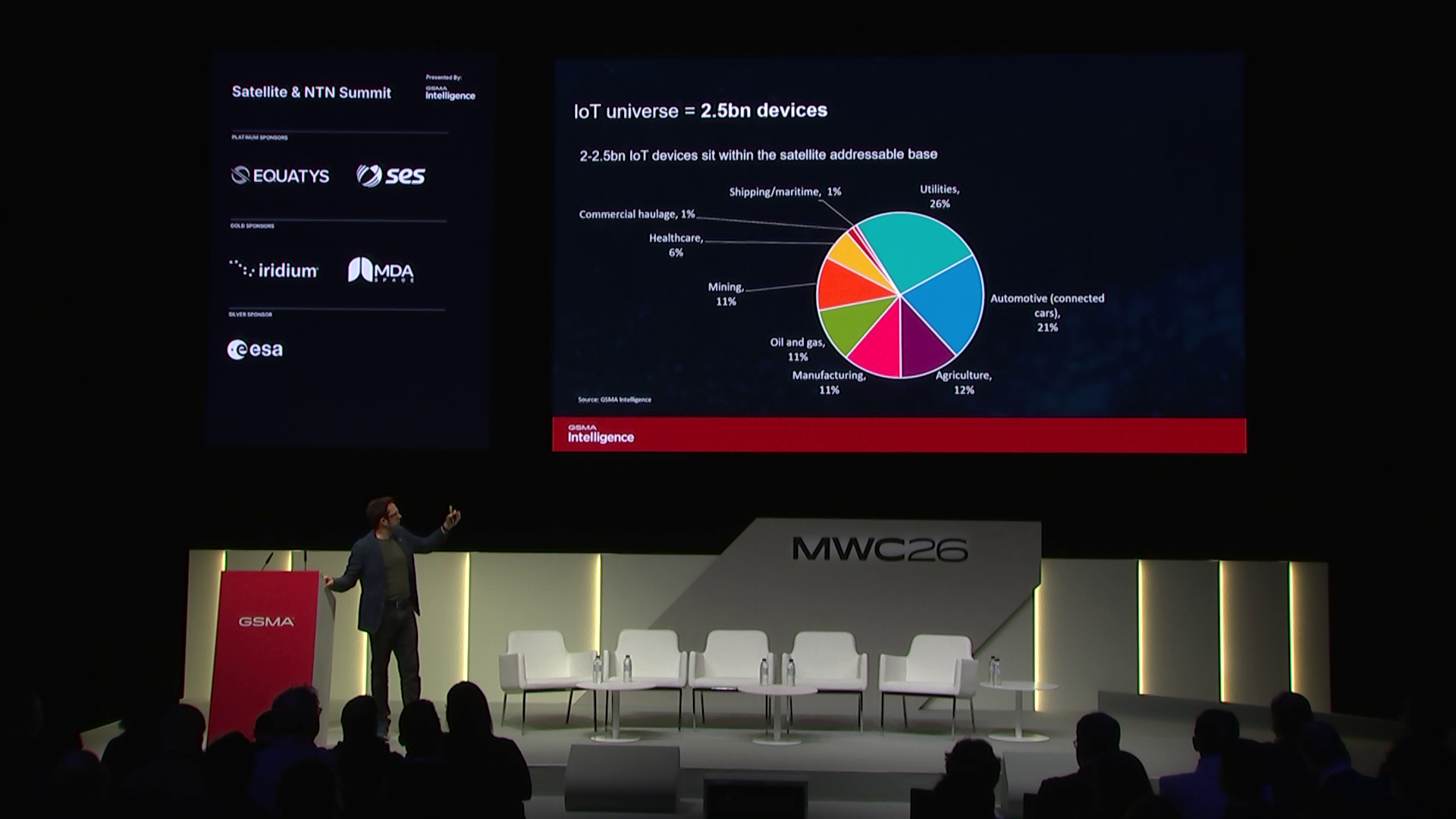

The headlines tend to focus on the massive opportunity in direct-to-device for smartphones – and while that story is real, the potential impacts for the IoT industry are equally game changing. GSMA Intelligence’s modelling puts the addressable base for satellite-connected IoT devices in the billions – 2.5 billion to be exact – by the mid-2030s. Their estimate of roughly $30 billion in annual addressable revenue by 2035 splits approximately 65% consumer and 25–30% IoT (with the remaining being Government & Defense) – and that IoT figure represents hundreds of billions in connected value across logistics, energy, agriculture, utilities, and more.

Critically, that forecast is underpinned not by optimism but by purchasing intent data from enterprise buyers, discounted for the reality that stated intent always outruns actual deployment. The survey data GSMA Intelligence presented showed the breadth of industries actively exploring satellite IoT – asset tracking, equipment monitoring, energy management, precision agriculture, and offshore operations among them – with no single vertical dominating. The directional signal is clear: IoT is a primary growth driver for satellite connectivity, not a secondary one.

2. Standards maturity is finally unlocking real scale economics

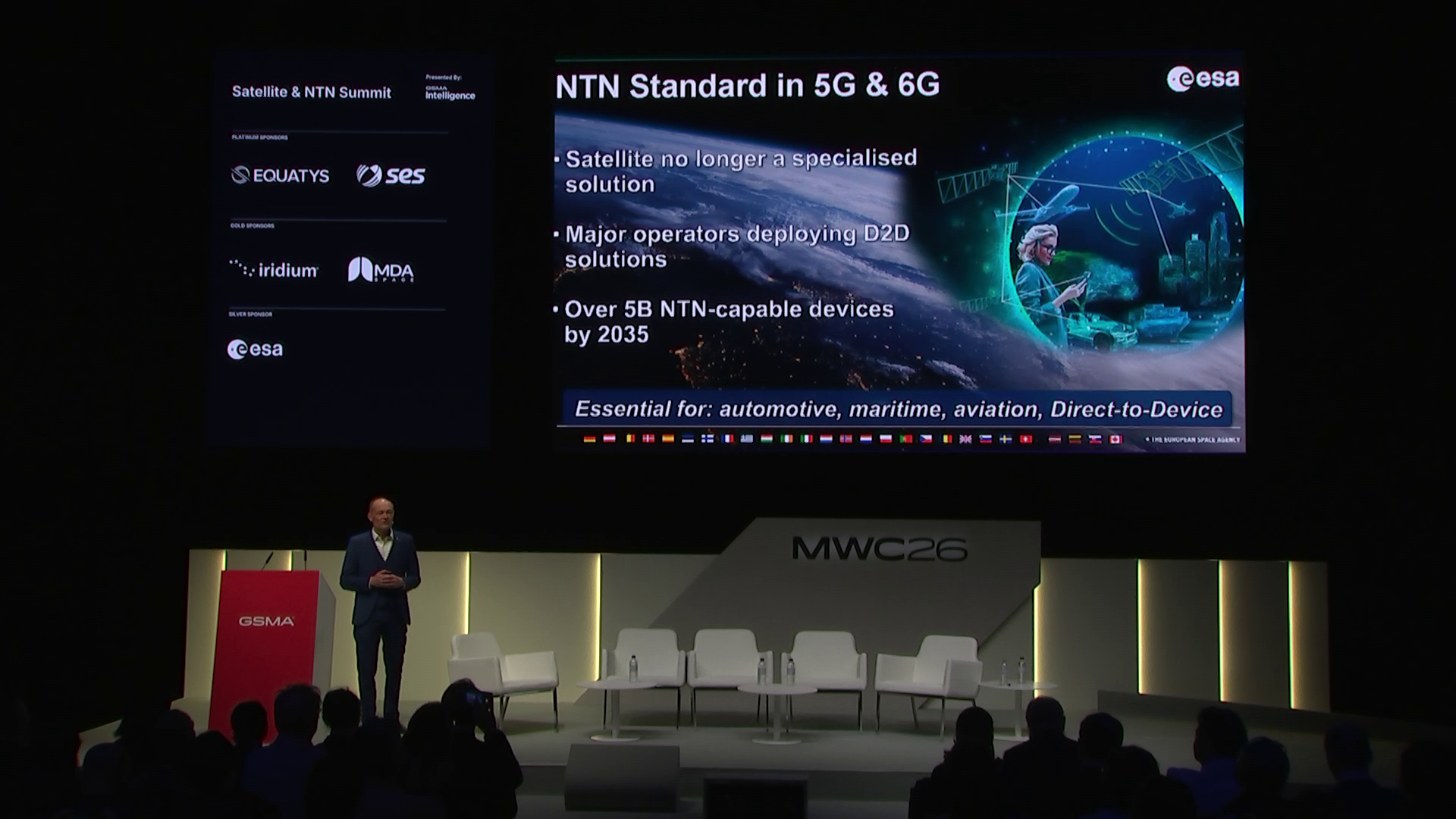

A recurring theme across the summit was 3GPP Release 19 – what it enables and why it matters. The European Space Agency’s Antonio Franchi was direct: NTN is no longer complementary infrastructure, it is foundational. And with each successive 3GPP release, that foundation becomes more capable. Release 19 is expected to enable regenerative payloads (effectively placing the base station on the satellite itself), improved power efficiency for IoT devices, new spectrum capabilities, and waveform optimisations that close the gap significantly with traditional satellite standards.

This matters for solution providers in a practical way: standardisation drives down cost and complexity across the entire value chain. When a single SIM card can roam between terrestrial and satellite networks using the same chipset and the same standards, the hardware burden on device designers drops substantially.

The GSOA’s Isabelle Mauro made the point clearly: the acceleration of innovation across the satellite sector in the past two to three years is unprecedented, and it spans all orbit types – not just LEO. Software-defined systems, inter-satellite links, and smarter spectrum utilisation are all driving capacity and efficiency gains simultaneously. For solution providers building on top of this infrastructure, the practical takeaway is that the cost and complexity curve is moving in the right direction, and moving faster than most expected.

3. Use case clarity beats technology enthusiasm – every time

This is where George Kanuck’s perspective at the summit deserves particular attention. Myriota has operated satellite IoT networks for a decade – outlasting many peers who came and went – and George was direct about why: our founders started with use cases at the edge, met with customers, and designed satellite performance around those use cases rather than the other way around.

That discipline – focusing on scale use cases that could sustain a profitable business through the development journey – is increasingly relevant as the NTN market floods with new entrants and investment. There is no shortage of satellite capacity being planned or funded. There is a shortage of deployments that reliably work for the end customer, at a price point that makes commercial sense, in the operational environments where connectivity gaps actually exist.

The GSOA reinforced this from the industry perspective: no matter how much progress is made at the standards or regulatory level, the end user is ultimately the critical decider. Seamless and affordable – those are the two criteria that will determine whether satellite IoT achieves its potential. For systems integrators, this translates to a concrete imperative: the differentiator is not access to connectivity, it’s the ability to match the right connectivity to a specific operational problem.

Asset tracking in remote mining sites, environmental monitoring in cellular dead zones, smart metering for utilities, and livestock management across vast rangelands: each has a different latency profile, a different data volume requirement, a different power budget. Selecting the right connectivity solution starts with knowing the use case precisely – and that knowledge is a competitive asset in its own right.

4. Partners are not just a go-to-market strategy – they drive innovation

A practically useful insight from George’s panel contribution addressed the nature of the partner relationship in IoT – and why Myriota’s operating model is built around it.

Myriota strategically operates as a vertically integrated stack, with ownership across spectrum, regulatory approvals, and satellite infrastructure underpinning our UltraLite and HyperPulse satellite connectivity services. Overlaying these services, Myriota provides an enablement layer of modules, dev kits, and edge devices – including products like the AssetHawk tracker and FlexSense sensing platform – that serve as the onboarding point for the partner ecosystem. System integrators and solution providers sit at the top of that stack, taking Myriota’s connectivity and reference hardware and adapting it to specific industrial use cases.

Our relationship with our ecosystem isn’t just commercial. Partners are actively shaping the product roadmap, with George pointing to the example of customer demand for lower latency and larger data packets being a direct input that drove Myriota to launch Hyperpulse, a 5G NTN network that now enables asset tracking, remote energy monitoring, water management, and oil and gas applications that require more detailed reporting and richer sensing. The innovation didn’t come from a technology roadmap drawn up in isolation, but rather from listening to what partners needed in order to serve their customers.

This is a model worth internalising. Systems integrators who think of themselves purely as resellers or channel partners are leaving value on the table. The ones who bring real operational problems from active customers are shaping next-generation solutions – and benefiting from a connectivity stack that evolves in response to what the market needs. In an industry moving as fast as this one, that kind of close feedback loop is a genuine competitive advantage for both sides of the relationship.

What to take forward

The summit’s closing panels converged on a consistent outlook: the next 12 to 24 months will see real commercial services in real markets, with genuine customer adoption across both consumer and IoT segments. The device and chipset ecosystem is also catching up, with Release 19 specs now flowing into hardware roadmaps. The European Space Agency’s announcement of up to €100 million in joint funding with the GSMA – targeted at 5G/6G hybrid infrastructure, D2D innovation, and AI-driven NTN optimisation – signals that institutional investment is accelerating alongside commercial deployment.

For systems integrators and solution providers, the window to develop genuine expertise in satellite IoT connectivity – to understand the technology, build the relationships, and develop deep use case knowledge – is now. The customers who will benefit most from this shift are already operating in remote, demanding environments. They need partners who have done the work to understand what “reliable, secure, and affordable” actually means when you’re connecting assets beyond the reach of any cell tower.

About Myriota

Myriota is a global leader in satellite IoT connectivity. Over the past decade, the company has built an expanding satellite constellation, secured a substantial patent portfolio of over 170 patents, and raised more than $100 million in funding. It now delivers both connectivity and hardware that underpin critical operations across agriculture, utilities, logistics, mining, environmental monitoring and defence.

Myriota enables systems integrators, solution providers and OEMs to easily develop and deploy connected products that sense, track, and monitor assets even in the most remote environments. With teams across 19 global locations and deep partnerships in key markets, Myriota remains focused on its mission to connect the physical world for impact.